Estate Planning BASICS: Trusts, Inheritance, Options, and Attorney COST

How to create, manage, and measure effectiveness in your Estate Plan

Estate planning can seem complicated and intimidating. It doesn’t help that the people who usually explain the process are attorneys, and sometimes it’s difficult to understand their legal lingo. We want to provide you with some valuable tips on how to create, manage and measure the effectiveness of your estate plan — in plain English.

Want an Estate Planning Guide that covers many unknown living benefits, but also addresses all common questions about planning for retirement? Check out our FREE eBook, The Ultimate Guide to Estate Planning (complete guide)

Below you will find an outline of estate planning insights from the ultimate guide that will enlighten you on some of the most important topics relating to estate planning.

Welcome to the ultimate guide to estate planning outline, brought to you by people who are not attorneys. We do not practice law, and we’re not telling you what to do. We are here to make things simple, explain terminology and provide you with important information. This knowledge will give you ammunition so that when you’re ready to consult with an attorney, an estate-planning professional or someone else who is setting up a will or a power of attorney for you, you will know what questions to ask. That will help you understand what you’re getting yourself into, who you’re talking to and what you need. Then you can make the best and most informed choices.

Most importantly, we want you to enjoy your retirement experience. Our goal is to provide you with what you need to know and what you need to find out. The more you know, the less intimidating the process will be.

What Is the Retire Happily Process?

We established the Retire Happily process to guide you in making financial decisions that align with your financial situation and goals. We are known for our ability to listen, understand and employ the optimum financial solutions and strategies that will give you the highest probability of enjoying financial freedom and the lowest probability of regret. We provide investment advice and insurance planning. We specialize in retirement preparation in areas you are probably concerned about and areas you might not even know to ask about. We pride ourselves on being thorough and on making complex subjects simple and easy for you.

We are here for you every step of the way. If you have any questions about any of our content feel free to contacts us to follow up.

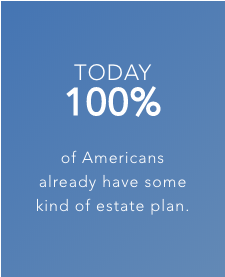

100% of Americans already have an estate plan.

- Either they made their own plan or a default estate plan was made for them by the state.

- This means that when you pass away, the state you live in has a plan for where your stuff goes.

Do you have a default estate plan?

58% of Americans 18+ have a default estate plan.

39% of Americans 37 – 71 have the default estate plan.

- 22% of Americans 72+ have the default estate plan.

What Is Estate Planning and Who Needs an Estate Plan?

If you have any assets at all, you need an estate plan. If you become sick or incapacitated (not able to do things because your mind is not right) and/or are unable to work, you will need someone who is legally allowed to help you. And when you die, you want your heirs — not the government — to get your “stuff,” your assets. It is critical that you do your estate planning while you are able. If you wait until you are sick, it is pretty much too late (more on that in the video).

All Your Stuff Legally

In the legal context, an “estate” refers simply to everything you own — your stuff. It includes your home, the things in your house, your car, your bank account, things you collect, things you cherish and your retirement accounts. Any account or asset you own is part of your estate.

Who Needs an Estate Plan?

Everyone needs an estate plan, even 18-year-olds, because once they are adults, no one else can make their medical decisions for them. They at least need to appoint someone to be their patient advocate to make decisions for them, if needed.

What Is Estate Planning Legally?

In the legal context, estate planning means you deciding what will happen to everything you own if you get sick and when you pass away. It is a legal process to take care of people and their property when they can’t do it themselves, either because they’re incapacitated or deceased.

Learn More: What happens to my assets when I die?

Without an Estate Plan?

Do you have a plan in place for when your family is faced with changes? If there is no estate plan, there’s no clear path of who will do what when the time comes. Who is going to make medical decisions? Who has the authority to pay bills? When there is no plan in place, the process will be confusing, costly and cumbersome. It will be a giant hassle, and you know what? It doesn’t have to be that way! The whole mess can be easily avoided with just a little bit of planning.

Some of the issues that pose the most challenges in estate planning:

- No Estate Plan in Place

- Problem with Putting Kids’ Names on Accounts

- Family Divorce in Your Estate Plan

- Disability Benefits for Your Child

- Managing Addiction in Your Estate Plan

Learn More: Challenges families face without an estate plan

Protecting Inheritance

An estate plan helps you manage/control your children’s inheritance. You’re able to decide who gets what, when and how they get it. You’re able to protect your kids or grandkids who have a tendency to spend too quickly or perhaps not make wise choices financially. You can set up a plan in advance for them so that it doesn’t end up being a hindrance to them.

Things you should think about relating to inheritance:

- Deciding Who Gets What

- Managing Assets for Your Children’s Inheritance

- Keeping Inheritances in Your Bloodline

- Appointing a Guardian and Trustee for Your Child

Learn More: How Does an Estate Plan Protect My Children’s Inheritance?

Urban Legends About Estate Planning and Probate

One of the biggest misconceptions about estate planning is that there is a magic form that applies to everyone’s situation that you can download from the internet. People think they can find such a form, fill it out quickly, sign their name, get it notarized and then everyone’s happy. If there were a magic formula, we’d like to think it is this educational series we put together for you to know what to expect, what to ask and whether you are using the right professionals for the job. It is true: generic forms do exist, but it is a risk to use them. Your personal form must be customized to address what is similar about your family situation and the unique aspects of your family’s situation.

The topics listed below come with a lot of misconceptions and “urban legends” related to estate planning:

How to Properly Customize Your Estate Plan Forms

Assets and Beneficiary Planning

Deciding Who Gets What in Your Estate Plan

Is an Estate Plan Just for the Rich?

Do I Need a Power of Attorney with All the Challenges?

Misconceptions About “One Size Fits All” Estate Planning

An Estate Plan You Don’t Need?

Should We Be Afraid of Probate?

What Are the Responsibilities of a Trustee?

Learn More: Common misconceptions about estate planning solutions and probate

Most-Asked Questions About Estate Planning

People ask many similar questions in slightly different ways about estate planning, and the answers to these questions can help you understand more about what may or may not apply. Preparing a list of questions for your estate-planning professional was the old way of getting the information you needed. Now you can simply watch a video to gather the right insights and be informed before you meet with anyone. Use the answers from the questions in this video as conversation ammunition when you meet with an estate-planning professional.

Knowing the different uses of a will and a trust will benefit you when you engage with an estate-planning professional. That’s just one example of how these insights can save you time and money and improve your chances of having an appropriately comprehensive plan.

We have made a list of the most common questions that people like you ask us about estate planning:

- Do I Need an Attorney to Help with My Estate Plan?

- Can I Change My Mind After I Set Up an Estate Plan?

- Do I Need an Estate Plan?

- How Do I Find a Good Estate-Planning Attorney?

- What’s the Difference Between a Will and a Trust?

- What Else Do I Need to Consider About Estate Planning?

- How to Store Your Estate-Planning Documents

- How to Protect Your Business with an Estate Plan

- Is There Tax Fees in an Estate Plan?

- What’s the Difference Between Life Insurance and Traditional Investing?

- What Do Savers Do with the Money They Have to Take Out?

- What Is a Living Benefit?

- How Does Elder Law Affect Estate Planning?

- Why Do I Need a Financial Power of Attorney in My Estate Plan?

- What’s a Fiduciary, and Why Should I Trust You?

- How to Prepare Funeral Expenses and Final Arrangements in My Estate Plan

- The Difference Between Traditional Life (or Death) Insurance and Corporate Design Life Insurance

Need answers to the questions above?

Learn More: Answers to the most-asked questions about estate planning

Trusts in Your Estate Plan

What Is a Living Trust, and when Is It Too Late to Get One?

A living trust is a legal document you make while you’re alive and well to take care of you, your family and your property if you become incapacitated temporarily or permanently. It makes sure your stuff goes where, when and how you want when you pass away. It’s too late to make a living trust if you’re not alive and well.

If I Have an Old Trust is it Garbage, or Can I Change It?

When updating or adjusting your trust, you have two options:

- In some cases, we can amend the trust, which is just a process where we change part of the language.

- If you have substantial changes, we might do a restatement of the trust, which is a total replacement, but we will use parts of your existing estate plan. Nothing is wasted.

Difference Between a Revocable Trust and an Irrevocable Trust

- The major difference is that you can’t change as much of an irrevocable trust as you can with a revocable trust. Even when a trust is irrevocable, parts of it can still be changed as needed.

- A revocable trust is the type of trust that can be completely changed and completely cancelled any time and for any reason.

There are different types of irrevocable trusts. They are created for larger estates, for estate tax-planning purposes and for unique family situations. Under current law, irrevocable trusts are used frequently for long-term care and nursing-home protection planning. This means you might be able to protect a significant portion of your wealth for your family.

When Would You Make an Irrevocable Trust?

These days, an irrevocable trust is created as protection mostly in two different situations:

- One is in a case in which someone is concerned about depleting his or her estate from long-term care or nursing-home costs.

- A second scenario in which an irrevocable trust is created for protection is when someone has a very large estate that would be subject to estate taxes when they pass away.

Important topics about Trusts you need to be aware of:

- What Is a Living Trust, and When Is It Too Late to Get One?

- Is My Old Trust Garbage, and Can I Change It?

- What’s the Difference Between a Revocable Trust and an Irrevocable Trust? What Can Be Changed?

- When Would You Make an Irrevocable Trust?

- Addressing Problems by Assigning a Trustee

- Mistakes That Trustees Often Make

- What’s the Advantage of an Attorney Who Specializes in Wills and Trusts?

Learn More: Trusts: definitions, problems, and differences in estate planning

Life Insurance and Long-Term Health Care

What do I need life insurance for at this age? Are you kidding me? I’m done working! Life insurance? Estate planning? That’s right.

What Benefits Come with Life Insurance in Estate Planning?

In estate planning, life insurance is one of the most powerful tools in managing your income taxes and getting benefits while you’re alive. If you encounter any type of challenges, either physically or neurologically, you can get benefits through very specific types of life insurance.

Two Activities of In-Home Daily Living

You can use these special types of life insurance for your benefit while you are living just because you are unable to do two of the six activities of daily living:

- Bathing

- Dressing

- Taking Medications

- Preparing meals

- Toileting

- Transferring

And you can use it at your discretion tax-free, which means you get to be the beneficiary of your own life insurance without dying.

Life Insurance Affects Estate Planning

Life insurance is important in estate planning, and you can use it to leverage your estate so you can leave more money to yourself while you are living and your heirs when you get your promotion in a more tax-efficient and protected way. If you are coordinating your life insurance with your estate plan, there will be no ongoing fees; your payment will be part of the one-time estate-planning fee. This may sound like the panacea of estate planning, and for about 70 percent of retirees, it can be. But (yes, there is a “but”) you do need to get an offer first from a life insurance company that specializes in working with retirees.

Long-Term-Care Expenses

There are two general approaches to planning in advance for the dreaded potential long-term-care expenses. Unfortunately, not many advisors are fully knowledgeable about these programs. Many are more focused on structuring their clients’ assets in stock market investments. Don’t get upset; they are doing their best. Many advisors have never been trained in this highly specialized area. What is worse, advisors who think they know how to use these more sophisticated methods can end up misusing great programs because they have little or no experience with them. We highly recommend that you investigate how this specialized Corporate Design Life Insurance can be a fantastic addition to a well-diversified plan, even if you don’t think you are interested.

Learn More: Life Insurance and long-term health care in your estate plan

Estate and Trust Types: What You Should Know About

Everyone needs an estate plan, and, as mentioned, everyone has one, even if it is the default plan created by the state they live in.

What Is the Default Estate Plan?

The default plan is what’s called “intestate succession.” This means a person dies without an estate plan, without any directions about how to handle his or her assets. That person doesn’t have a will or a trust, and no one legally knows exactly what to do, so the government tells the family what to do. All the stuff has to go to court. If you die without an estate plan you set up in advance, the government will decide where your assets will go, who’s the next of kin, who your creditors are and how much you owe them. You can avoid this easily. It is not funny, but those who fail to plan will plan to star in their own horror film of trying to live peacefully and get their stuff where it belongs.

Estate Plan Objectives

The basic objective of an estate plan is to get your stuff where it belongs for your benefit while you’re living and also when you pass away. There are many different options and paths when building your plan.

These are the main options with trusts and estate plans:

- The Default Estate Plan

- Do-It-Yourself Beneficiary

- Transfer on Death

- Durable Power of Attorney

- Medical & Financial Power of Attorney by a Professional

- Do It Your-Self Estate Planning

- Last Will and Testament

- Revocable Trust

- Irrevocable Trust

- IRA Trust

- Special Needs Trust

- Medicaid Trust

To learn more about the different types of trusts and estate plans, read our full-length article, with video included.

Learn More: Different estate and trust types: simple explanations and examples

Building & Adjusting Your Estate-Planning Goals

What if you need to adjust your estate-planning goals or your needs change? What do you do now?

Adapting to Changes

Here’s the obvious: if you have a change in your family, health or wealth situation, go back to the attorney who drew up your documents, and have him or her make the needed revisions. If you change your estate-planning goals, make sure all your documents reflect your current wishes.

Once you Fund a Trust is it Forever?

People often ask if they can change their minds about details once they have completed funding a trust. The answer is Yes, you can always change the trust but, there are many options to consider.

After Trust: What’s Next After Setting Up a Trust?

People try to do the right thing by setting up a trust. Is that all they need to do? No. When you set up a trust, there are still things that need to be done. First, while you’re able, make sure you align your financial plan with your estate plan. It is important that you have a plan in place that is appropriate for your age, needs and preferences. You can have the world’s best estate plan, but if it is not fully aligned with your financial plan, all that work on the estate plan might not matter too much.

How Often Should I Review My Estate Plan?

Once you have your complete plan set up by a specialized professional, review that information every five years to make sure it’s up-to-date with current laws. If anything changes in your family situation, health or wealth, you should review your legal documents to be sure everything is up-to-date.

How Much Does Estate Planning Cost?

Preparing an estate plan can cost anywhere from $500 to $10,000. It costs between $350 and $650 to have an attorney draw up financial and medical durable powers of attorney. You can estimate that it will take an attorney typically one to two hours to review any previously established documents. So depending on his or her hourly rate, you can figure the costs.

Learn More: How to evaluate estate Planning cost of an attorney vs. value

What Are Your Options After Learning the Basics of Estate Planning?

Now that you have gone through all the information about estate planning, you are probably wondering, “What’s next? How do I turn this information into insights that can help me prepare my estate plan?”

Download the Retire Happily Estate Planning Book

‘The Ultimate Guide to Estate Planning‘.

This free educational ebook explains estate planning as simple and complete a possible.

Ready for a Financial Professional?

Okay, so you’re officially fired up about estate planning, but maybe you’re unsure about how to get started. No problem! We understand that all the information involved in estate planning can be a little intimidating at first.

- Do you have questions, comments or suggestions after viewing our Estate Planning Guide?

- Would you like to video chat or talk on the phone to someone at FundMax before meeting with an attorney?

- Would you like us to recommend an estate planning professional?

Referrals for Estate Planning

If you’re looking for a referral from a tax or legal professional, we will refer people to you if we’re comfortable with them and if we and our other clients have had good experiences with them. We will not refer anyone to you if we are uncomfortable about doing so.

You might need us, but you might not. Maybe you came here and got all the information you need, and you are thinking, “I feel a little guilty because I got all this stuff from them and gave them nothing.” Well, share it. Send it to somebody else…or don’t. We are here for you. We are here for your benefit, so feel free to use all our materials to learn something new. We will be here, still serving you and giving you information.

If you have questions you would like to have answered that you think others might benefit from as well, contact us, and we will likely create a method to answer those questions as well. You are probably not the only one with that question.

This is a resource we have developed for you, for your benefit. Make no mistake, we are a thriving financial firm that makes money. We are a financial firm that takes new clients. But first and foremost, we consider ourselves a significant resource to the public…mostly people we will never need to meet. We believe in providing you with valuable information at no charge. We know it can be intimidating to ask someone for help, especially if you’re a do-it-yourselfer or if you feel like you’re all set. We are here for you as a resource, and we get a lot of clients as the indirect result.

Thank you so much for viewing, for sharing, for engaging, for benefiting. It’s all for you.